The Market

Demand for Aggreko's services is created by events: our customers generally turn to us when something happens which means they need power or temperature control quickly, or for a limited period of time. Events that stimulate demand range from the very large and infrequent to the small and recurrent.

Examples of high-value, infrequent events or situations we have worked on include:

- Large-scale power shortage – South Africa, Bangladesh, Argentina.

- Major sporting occasions – Olympic Games, FIFA World Cup, Asian Games.

- Entertainment and broadcasting – Glastonbury, Ryder Cup.

- Natural disasters – Hurricane Sandy in North America in 2012, Brisbane floods in 2011.

- Post-conflict re-construction and military support – Congo, Iraq and Afghanistan.

Examples of lower-value, more frequent events on which we might work are:

- An oil refinery needs additional cooling during the summer to maintain production throughput.

- A glass manufacturer suffers a breakdown in its plant and needs power while its own equipment is being repaired.

- A city centre needs chillers to create an ice-rink for the Christmas period.

HOW BIG IS THE MARKET, AND WHAT IS OUR SHARE?

Because we operate in very specific niches of the rental market – power, temperature control and, in North America only, oil-free compressed air – and across a very broad geography, it is very difficult to determine with any accuracy the size of our market. A complicating fact is that our own activities serve to create market demand – Mozambique and the Ivory Coast did not figure highly in our estimates of market size a few years ago, but they are now important customers as a result of our sales efforts. Furthermore, our market is event driven, and major events such as hurricanes in North America, the Olympic Games, or major droughts in Africa can influence local market size in the short-term.

We have tried all sorts of ways to size the market for the Local business. In large and mature markets this is difficult, but not impossible. We can seek to track down every competitor and guess how much they have on rent as opposed to us. In emerging markets, where we are growing fastest, estimating market size is not difficult, it is impossible, as we are often the only major player in the market and the job we do is one of demand creation. Until we arrived in, say, South Africa, there was no market for industrial-scale temperature-control rental, because nobody offered it. Now there is one, because we do. So our approach is what expensive (and therefore, presumably, clever) consultants tell us is called 'market potential estimation', which works as follows:

- Step One: in a market (say, oil-refining in the US) in which we are well-established and have high market share, calculate our rental revenues (a known number) in the sector as a proportion of the total economic output of oil refineries in the US (another known number). This produces a very small number, like 0.00001.

- Step Two: make the bold assumption that if we can achieve, say, 0.00001 of the economic output of refineries in the US as revenues, we should, in theory, be able to achieve the same in oil refineries everywhere else. Therefore if we take the total economic output of oil refineries in, say China, and then apply the same multiple to that which we achieve in the US, that tells us how big the potential market is, and how little we have, so far, achieved in our attempts to penetrate Chinese oil-refineries.

- Step Three: take this same technique, and apply it to about 20 segments in 30 countries, and, heypresto, we have a number for the market potential (a dodgy number) and a number for our revenues in the sector (an accurate number), and therefore an estimate of our share of 'market potential'.

This is all a bit flimsy but, absent spending a fortune of our shareholders' money on consultants, it is the best that we can come up with and, actually, and most importantly, it is a useful technique for our salespeople because it tells us pretty accurately which markets and sectors we should be concentrating our efforts on.

From this process, we have come to the following conclusions:

- We estimate that our worldwide market share is around 25%. Given that we have Local business revenues of £904 million this would imply Local 'market potential' of about £4 billion.

- In almost every country we operate in, we are the number one or number two player, and we are the only competitor that operates in all major regions of the world.

- The Local business market is growing at about twice the rate of GDP, and probably faster than that in some emerging countries where the market barely existed before we turned up.

Estimating market size is easier in the Power Projects business because there are few competitors, and we get reasonable intelligence about their activities. We estimated that the total market for Power Projects in 2012 was about 8,400MW +/–10%. Our average MW on hire in 2013 was 3,700MW, which says that our market share was around 45%.

WHAT DRIVES GROWTH IN THE LOCAL BUSINESS?

Growth in Aggreko's Local business is driven by three main factors:

- GDP – as an economy grows, so does demand for energy in general, and rental equipment in particular. When economies are growing fast, businesses tend to be busy, and they are therefore more likely to rent power equipment for a weekend to do necessary maintenance, rather than lose production. In slow-growing economies where there is excess capacity, the reverse is true.

- Propensity to rent – how inclined people are to rent rather than buy. This is driven by issues such as the tax treatment of capital assets and the growing awareness and acceptance of outsourcing. In emerging markets, financing is hard to come by and often exorbitantly expensive, and they are therefore more likely to be prepared to rent.

- Events – high-value/low-frequency events change the size of a market, although only temporarily. For example, Hurricane Sandy in 2012 led to a shortterm surge in temporary power demand in the areas affected by the disaster; likewise, the London Olympics in 2012 vastly increased the market for power rental in the UK, but for six months only.

In the five years to 2012, real global GDP grew by around 1.7%; so we would assume that the market potential grew by around 3.4% in real terms. During the same period, our revenues in the Local business grew by 15% in nominal terms, and by 10% in constant currency terms. This is evidence that we have substantially and successfully increased our market share in the Local business over recent years.

WHAT DRIVES GROWTH IN THE POWER PROJECTS BUSINESS?

The factors which drive the growth of our Power Projects business are different. The main trigger of demand is power cuts; when the lights go out in a country, people want power restored as quickly as possible. It is a perverse fact that people value power most when they are without it. We believe that in many parts of the world, and most particularly in many developing countries, there will be increasing numbers of power cuts, caused by a combination of burgeoning demand for power, ageing existing plant and inadequate investment in new capacity.

It is worth understanding how whole countries can run short of power, and how this expresses itself. First, for the lights to stay on, power production must exactly equal power consumption; in developing countries there will be peaks of demand in the early morning and in the evening, and troughs at night; and there is often a seasonal pattern – in summer people turn on air-conditioning and large amounts of extra demand can come onto the system. A country needs to have enough generating and transmission capacity to cater for the absolute peak demand, plus a safety margin (called the 'reserve margin') to cater for unexpected breakdowns and scheduled maintenance. If a country does not have a big enough reserve margin, power cuts inevitably result. These typically first show at times of peak demand; as the gap between supply and demand grows, so the frequency and duration of power cuts increases. In the early stages of power shortage, power cuts may be rare, seasonal, and bearable. But as the reserve margin drops, they become more frequent and disruptive and start to have very serious impact on the economy and life of a nation. In countries such as Tanzania, Pakistan and Venezuela people can be without power for as much as 12 hours a day, and the World Bank has estimated that the average sub-Saharan business can be without power for over 50 days a year.

The reserve margin is a simple function of supply and demand. In our core market for Power Projects both of these factors are conspiring to reduce reserve margins; economic and population growth is driving increasing demand, and lack of investment in new and existing generation means that supply cannot keep up with demand.

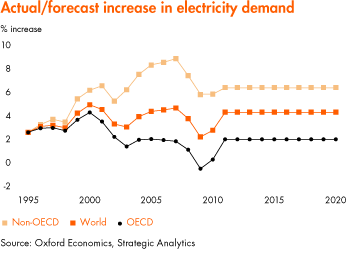

Our core market for Power Projects is in emerging markets where GDP is growing fast, and demand for power is growing faster than GDP. Working with a leading group of professional economists at Oxford Economics and Strategic Analytics, we have built models which take data on GDP and population growth, power consumption and power generation capacity for 170 countries over the last 10 years. Using this historical data, we then project future power demand based on forecasts of population and GDP growth. Our model predicts that worldwide demand for power will grow by around 4% per annum between 2010 and 2020, comprising around 6% in non-OECD countries and 2% in OECD countries. Our model reflects the sharp divergence between the growth in power consumption between OECD and non-OECD countries in recent years, as shown in the graph below.

The rapid growth in power consumption in developing countries is driven by industrialisation, urbanisation and by the growing number of consumers having access to devices which consume electricity, such as fridges, televisions and mobile phones. Between 2000 and 2010, the number of people whose power consumption per capita was growing faster than per capita GDP increased by nearly 1 billion to over 3 billion souls (source Oxford Economics). And, according to the International Energy Agency, there are still over 1.3 billion people with no access to electricity. This is not through lack of wanting.

To make this situation worse, by 2015, around 25% of the world's installed power-generating capacity will be over 40 years old, which we believe is a reasonable proxy for the average life of a permanent power plant. The coming years will see the beginning of a replacement cycle during which a large part of existing power-plant construction capacity will be dedicated to replacing existing plants in North America and Europe, rather than building replacement or additional capacity in developing countries. The sums which need to be mobilised over the next 10 years to re-build the power distribution and generation capacity in North America and Europe are huge; in the UK alone, the regulator estimates that up to £150 billion will be required. This means that developing countries will have to compete for funds with developed countries, where investment risk is perceived to be far lower.

As part of our recent Strategy Review we updated our current models of the gap between supply and demand, and we now believe that the combination of these demand-side and supply-side factors will increase the worldwide shortfall of power generating capacity to around 230 gigawatts (GW) by 2020 which is a nearly 4-fold increase from 2005 when it was about 63GW. In our core market, which we define as non- OECD countries excluding China, we estimate that in the same period the shortfall will increase 9-fold, from 29GW to 195GW. The ultimate size of the shortfall will depend on both the rate of increase in demand and the net additional generation and transmission capacity brought into production during the period. Even if the shortfall is lower than our current forecasts, it will still represent a level of global power shortage significantly larger than today's. We are confident that such a level of power shortage will drive powerful growth over the medium and long term in demand for temporary power as countries struggle to keep the lights on.

We are sometimes asked whether the drivers of growth in Power Projects are 'cyclical' or 'structural'. The answer is that one is affected by the other; the immediate force of the structural drivers is affected by the economic environment. In the long-term, the drivers of growth – increasing demand for electricity and inadequate investment in supply – are structural. But the decision to spend hundreds of millions of pounds on sustaining electricity supply using temporary solutions is in most cases a political one.

The budgets of utilities in developing countries are generally controlled by government, and money spent on temporary power is money that has to be diverted from elsewhere; the easiest, simplest thing to do is to just put up with power cuts and not spend the money. Only when the pressure becomes intolerable will the coffers be opened. Intolerable pressures include demands from industry and commerce desperate for power, and from voters angry about lack of power. The balance of pressure and availability of money are both affected by economic circumstance and sentiment. If economic growth is strong and tax revenues are growing; if industrial activity is expanding, and deficits under control; if debt is cheap, then customers will be more inclined to spend money on temporary power. This was generally the case in the decade up to 2012. In the last two years, economies in emerging markets have seen lower rates of growth and greater uncertainty, and accordingly the willingness and ability of governments to spend money on temporary power has been tempered.

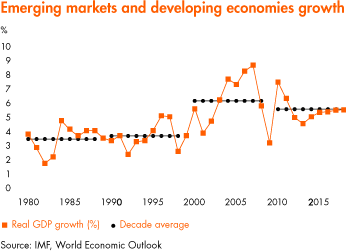

Whilst we are not economists, we do sometimes listen to what they say, and the consensus seems to be that the next five years will see real GDP growth rates in emerging markets that are around 5.5%, about 1 percentage point less than in the period 2000-2010 (see graph). It is because of this that we have reduced our forecast of average growth in demand for temporary power over the next five years in this sector to be in the range of 10-15% rather than the 20% we saw in the last five years.

HEALTH WARNINGS

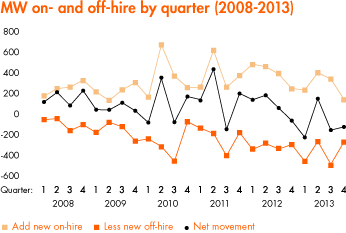

Our Power Projects business has delivered impressive returns over the last two strategy cycles: a compound growth of 34% in trading profit and an average return on capital of 31%. Because the structural drivers of growth are so strong, it is easy to be seduced into the belief that progress has always been smooth. This is not the case: not only has order intake been volatile, but we have also seen large variations in quarterly onand off-hire rates (see graph below). In a business where customers pay a premium for the ability to take on or get rid of capacity at short notice, we should not be surprised if they exercise their rights for their convenience rather than ours, and it is therefore the case that growth in our Power Projects business is subject to fits and starts rather than one of smooth progression. The structural growth drivers will ensure that, over time, the direction will be onwards and upwards but, from quarter to quarter and from year to year, it will not be a smooth ride.

It is also important to remember that Power Projects specialises in providing energy infrastructure in countries where political and commercial risk is high – sometimes very high – and the fact is that we do business where others fear to tread. To date, we have never had a material loss of equipment or receivables but it is likely, that sooner or later, one of our customers will misbehave. Our assets are at much greater risk of loss or impairment than they would be if they were sitting in the suburbs of London or New York or Singapore. We have extensive risk-mitigation procedures and techniques, and we are currently carrying £49 million of bad-debt provisions, but investors should remember that the returns we report are fundamentally 'risk-unadjusted rates of return' because nobody has yet behaved badly enough to adjust them.